In an Atradius survey of businesses in western Europe, respondents said that economic conditions such as inflation and higher costs of funds were having a negative impact on them.

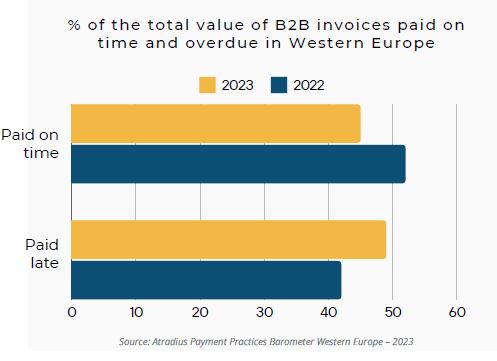

Many businesses reported finding it difficult to pay their bills at all. In fact, nearly half (49%) of the total value of B2B payments were paid late,

while only 45% were paid on time.

A separate survey by Intrum found that 37% of businesses in Europe pay their suppliers later than they would accept payments themselves. And more than half of European businesses said they would like to pay invoices faster but didn’t feel doing so was currently feasible.

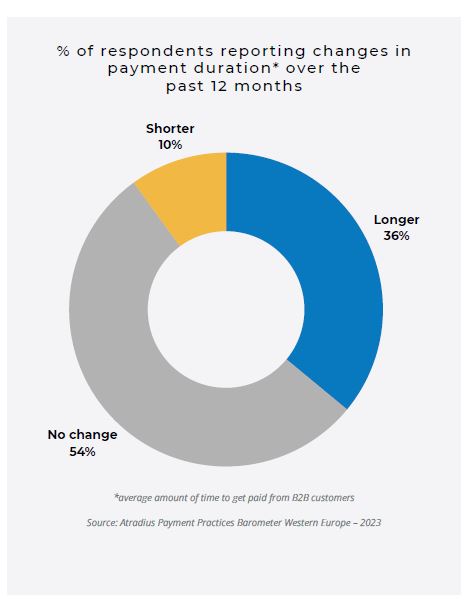

Businesses are coping with this uncertainty by focusing on their working capital. This means that buyers are trying to extend their terms so they can keep their cash available longer. Suppliers, on the other hand, want to get paid as quickly as possible.

“Buyers are also looking to expand their DPO (days payable outstanding) using card payments. So they’re working out an arrangement with the supplier to offset part of the card fees.”

These sorts of arrangements are helping card payments to offer more benefits for both parties, Stynen said.